The Banking as a Service market in the US is taking off. Banks, however, commit the classic blunder of adding another new layer on top of an already patchwork legacy technology platform. Banks are bringing in innovation through middleware on top of the legacy core.

Certainly, this model enables banks to launch BaaS more quickly, but the component executing backend processing is still the legacy core that was designed for customers’ needs of yesteryears, and cannot cater to the agile and real-time needs of the embedded finance market. The metamorphosis of the legacy core during these years has not gone beyond automation of manual work - moving from paper ledger to mainframe ledger, automating money withdrawal from teller station to ATM, balance checks from branches to online, and deposit capture using mobiles. Years of evolution have resulted in complex mainframe architectures with layers of transformation to automate work previously done by humans, turning the architecture at banks look like Frankenstein’s monster as shown below.

Rabo Bank's technology architecture (Source: Finextra)

On one hand, banks complain of core dependency that hampers their ability to innovate, but continue to follow the dreaded path of layering and patching up in response to BaaS. While this model certainly works to launch BaaS, it doesn’t meet the demands of the other participants in the financial ecosystem.

The expectations of all participants in the financial ecosystem are benchmarked against what’s trending with today’s technology, as against what 40-year-old mainframes can deliver. Today’s technology has democratized affordability and apart from creating a level-playing field, it is also setting new benchmarks of service. To name a few, customers enjoy the

Freedom from expensive hardware cost

It took over 6 months to install a server 10 years ago, but the same takes less than an hour with Amazon, Azure, or any cloud provider today. Today it is now 100 times cheaper and 1000 times faster than what it was 10 years ago.

Freedom to have a CRM system

20 years ago, good CRM software was affordable only to enterprises that could spend hundreds of thousands of dollars. But today, even a small business can get the same sophisticated CRM in less than 5 minutes for a couple of hundred dollars.

Banking is no exception - it’s time to reset

It's time banking technology is reset to provide the cost-effectiveness, ease, and agility for adoption, especially at a time when banking services are the hidden challenges, being at the core of a changing financial ecosystem.

So, what are the options for banks?

1. Replace the core?

A high-risk, complex, and cost-prohibitive option, banks should not waste time and money to rip and replace their legacy core. Allow the workhorses to chug away with just delivering what they were designed to do, without saddling them with the demands of today’s embedded finance.

2. Wait for the core provider to step up?

Dependence on legacy core providers doesn’t allow banks to benchmark their transformations against challengers, but rather limit them to the precincts of the often sluggish and organic innovation strategy of their core providers. Decades of patient waiting, exponential costs, and awkward contracts have left banks tired of waiting, gradually losing market share in the new landscape.

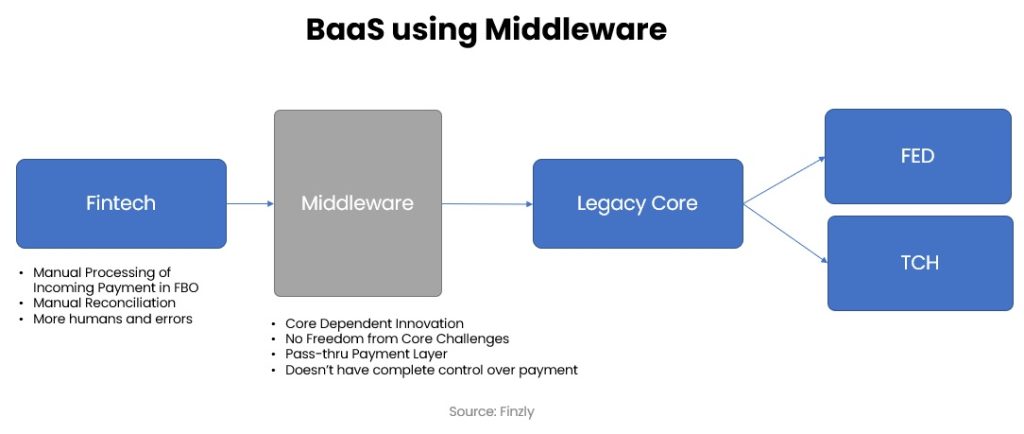

3. Add a middleware layer?

Adding a middleware layer still uses legacy technology that needs feeding and watering, and above all, it limits the bank to what the legacy core offers. It just knits together different silos of the bank and allows it to talk to the underlying legacy core. Banks are still left with stranded data in unusable formats, spawning unnecessary maintenance costs and overhead.

Then what is the right model for BaaS?

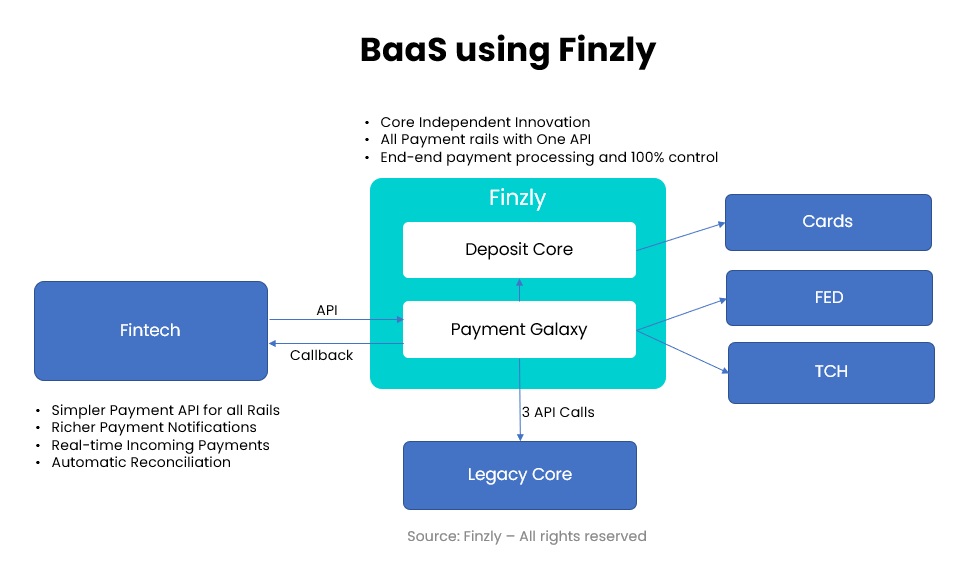

Without ripping and replacing the core, banks can launch a parallel digital core in the cloud in less than an hour, a thousand times faster than a typical 2-year core overhaul project, above all, at a much lower cost. Finzly’s digital core and Payment Galaxy, the payment hub, with pre-built connections to the Federal Reserve (ACH, Wires, and FedNow), The Clearing House (RTP), SWIFT and card networks, along with customer onboarding, KYC, OFAC, Fraud management, Workflow controls, Audit, and End-user Experience components, are available to launch a new bank in less than an hour. It is as simple as building your dream house with Legos.

Finzly’s approach is to bypass the core for any innovation, so you can simply build your new modern home adjacent to it. Finzly offloads the workload from the legacy core, unlike middleware used in BaaS, which still turns to the old and tired legacy systems for backend processing. Processing payments and deposits outside the legacy core saves banks from having to pay for each statement, account, card, and other bells and whistles. With no more dependency on the core providers for innovation, banks can confidently offer APIs to talk to other vendor applications, Banking as a Service APIs to fintech partners, virtual/FBO accounts, operated outside the core with only 3 lightweight API calls to the legacy core.

Why is this model great for banks?

1. This model simplifies the payment experience for customers, giving them a FedEx experience of only having to worry about the speed and cost of moving money. Based on these priorities, Finzly routes the payments smartly through the most appropriate payment rail that meets the customers’ priorities.

2. With the payment processing offloaded from the legacy core, banks can enjoy from instant adoption of payment networks of their choice. Recently, Finzly launched wires on our digital core for one of the banks, and eventually, when the bank wanted to add the ACH rail, it took just a day to get the ACH service set up. When FedNow is up and running, the bank needs just another day to bring the service to its customers. Banks queueing up with their core providers to connect to Zelle cannot cater to the demands of 82% of Americans already using digital payments. Banks need the power of technology that can bring alive payment rails and fintech partnerships in a day.

3. Banks don’t have to deal with multiple payment systems, one each for ACH, wires, RTP, Swift, FedNow, etc. with each connecting to Core, AML, Fraud, Risk, GL, Warehouse, and several other various other payment eco-systems. All payments, irrespective of the rails, are processed and available in one payment hub, with a single connection to the eco-systems, offering straight-through processing, saving costs, and increasing efficiency.

4. As Finzly’s platform comes with Banking as a Service APIs out of the box, there is no need for another middleware provider, cutting down cost, reducing manual tasks, increasing efficiency, and making the technology stack simpler.

5. Fintechs can eliminate the manual processes around incoming payments, incorrect routing, errors, and repairs as the Finzly platform provides rich information to fintechs via webhooks, enabling them to post the incoming credits in real-time.

6. Banks can create digital wallets in any asset class – be it USD, foreign currency, crypto, or reward points. The multi-asset, multi-currency ledger is built for the economy of the future.

7. Banks can become the ledger for the fintechs allowing them to access the accounts using APIs, or simply operate FBO accounts letting the fintechs maintain their own ledger.

8. Transferring assets from one class to another, buying/selling foreign currency and managing P&L of these assets is critical to the global treasury and the crypto world. The cross-asset foreign exchange module that is pre-built within the platform seamlessly offers these capabilities.

9. Finzly’s customer experience platform can easily overlay on the new modern capabilities built by the bank. Customers can simply single sign-on from the current digital login to Finzly’s customer experience platform.

10. Customers can have multiple levels of parent-child relationship allowing the parent entity to manage the child entities without multiple entity level accounts.

Conclusion

With banks already spending up to 80% of their budgets on maintaining legacy technology, offering BaaS using middleware is another addendum to the cost of upkeep, especially considering the scale and volume of customers and transactions that BaaS could potentially bring in to the banks. With vendors presenting multiple choices to banks, few far-sighted banks have hired Heads of Innovation/ Banking as a Service/Strategy who really understand the pros and cons of each model. It is wise for the banks to choose a model that is simple for customers, easy for bankers, faster to go to market, cost-effective, above all good for the long-term health of the bank!

Explore our Digital Core that's helping banks launch Banking as a Service.